Mercer actuary David Knox says the data used to determine the old age dependency ratio is “totally out of date” and overstates the severity of the problem.

From their inception, SMSFs have always attracted more than their fair share of criticism. Now it’s an ageing membership that’s being used to restrict their numbers.

ASX ahead for third week, RBA bond market intervention

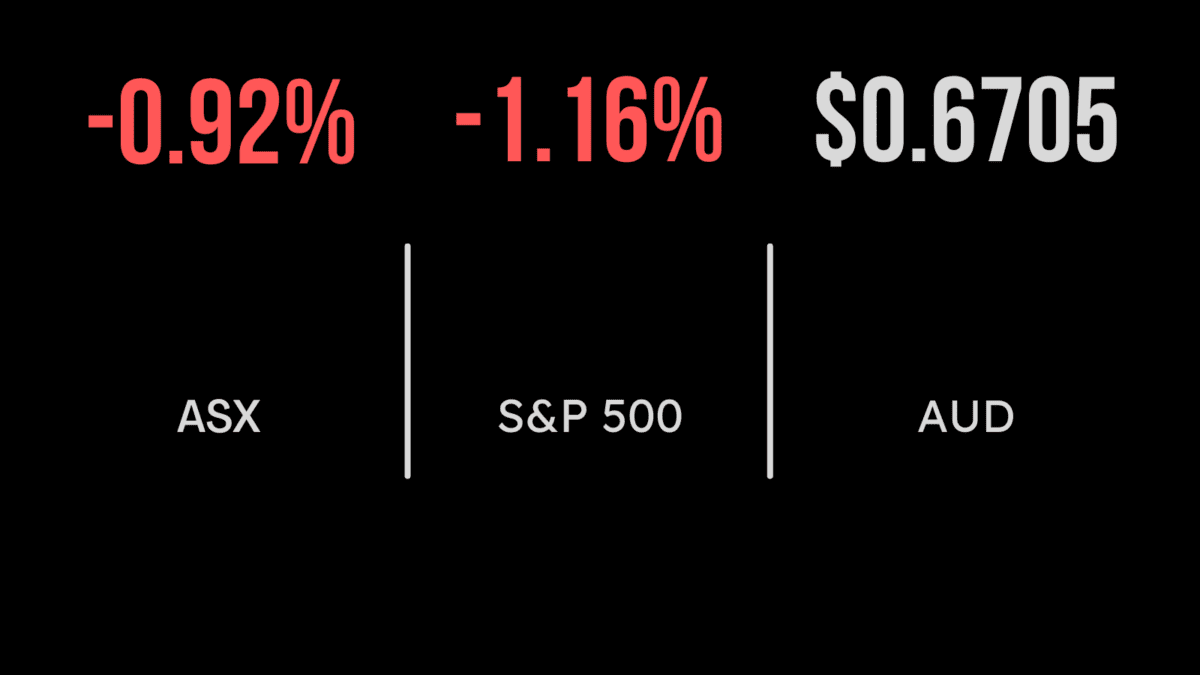

ASX finishes flat, but back to September high, RBA gets busy, Wesfarmer’s robust

The S&P/ASX200 (ASX: XJO) finished flat on Friday with strength across most consumer facing sectors including discretionary (1.4%), staples (0.9) and property (0.7) offset by another sharp selloff in energy companies, which were down over 2% as reality kicked in about the oil ‘shortage’.

The RBA had a busy day, announcing they believe it is in the best interests of the retail market for BNPL players including Afterpay (ASX: APT) to remove the contractual terms that restrict the retailers they work with from passing their cost onto the end consumer.

Despite the potential for a significant impact on profitability, shares fell just 0.3%.

The bank also doubled down on bond buyer, effectively confirming their intention to keep rates below 0.1%.

Aurizon (ASX: AZJ) announced a plan to acquire One Rail from Macquarie Group (ASX: MQG) for $2.35 billion, shares fell 6% on the news and were down over 7% for the week.

Rare earths darling also bore the brunt of COVID shutdowns, falling 8% on Friday after announcing a 30% fall in sales in the quarter.

Over the week the ASX gained 0.7%, behind strong performances by Wesfarmers (ASX: WES) and Macquarie Group (ASX: MQG), the two Australian powerhouses gaining close to 5%.

WES highlighted robust sales at Bunnings despite challenges at Target and KMART, whilst Macquarie took the crown as the most profitable investment back in a bumper year that has shares nearing $200.

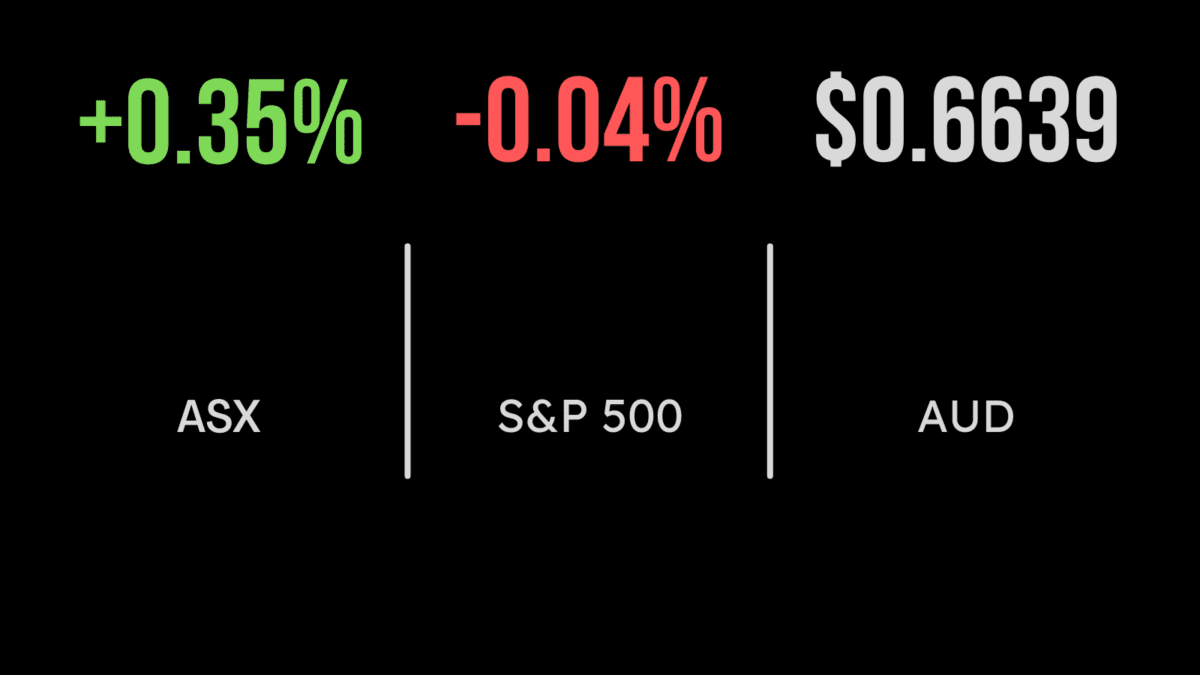

Dow finishes at record high, Snap cracked, Intel misses on growth

The Dow Jones finished at its first all-time high in over a month, gaining another 0.2% taking the weekly return to 1.1%.

The S&P 500 and Nasdaq both underperformed, down 0.1 and 0.8 respectively with the technology sector taking a hit from Snapchat’s (NASDAQ: SNAP) weaker than expected update. Over the week, however, it was all positive with both indices gaining over 1%.

Returning to earnings season, social media platform SNAP was down 26% in Friday’s session after management complained about Apple (NYSE: AAPL) implementing new privacy measures.

According to the announcement, the new security changes mean advertisers can no longer target individuals as closely as before.

They also flagged a falling spend in advertising on the back of supply chain disruptions and a lack of product.

Intel (NYSE: INTC) also fell by 11% as their revenue and data centre sales came out worse than expected.

The company continues to deliver profit margins exceeding 50%, however which drove a 50% increase in quarterly profit.

Data centre chip sales were 10% higher, but below expectations given the importance of the sector for their future growth. Revenue improved more mature 5%.

In political news, President Biden confirmed at a Town Hall meeting that he may struggle to deliver the corporate tax increases he hoped, buoying the market.

Raising rates, Tesla, Netflix and the power of earnings, regulatory expansion

The financial media remains obsesses with the threat of inflation and near certainty that is higher interest rates, and they may well be right at some point in the next decade.

The concept of ‘transitory’ vs. ‘persistent’ inflation is being discussed with vigour yet most continue to ignore the fact that we are exiting a near two-year pandemic.

The pandemic shutdown effectively broke supply chains for an extended period, so expecting they would not be an issue when life returned to normal is clearly naïve.

What happens next is anyone’s guess, but as supply and demand rebalances, we may well head back to the deflationary environment we had before; in this environment the early raises of rates would hurt the prospect of recovery.

When investing into equities, earnings are ultimately the driver of shareholder returns, not income.

If a company is consistently growing earnings over time, they will be worth more over time.

The US quarterly reporting season is reiterating this, with some 85% of the 70 odd companies that have reported thus far easily exceeding even heightened expectations.

Importantly, just relying on those companies whose earnings benefit from a cyclical increase in the price of the goods they sell simply won’t deliver sustained returns, but those providing services or building customer loyalty clearly will.

Both Tesla and Netflix proved this and reiterated the importance of having global equity exposure within portfolios.

Tesla delivered record profits and overcame a chip shortage to expand vehicle deliveries, whilst Netflix saw some 150 million customers watch Squid Game and another 4 million sign up to their platform.