It can be hard to find good films starring older actors and about retirees. But it’s worth the reward when you find them. Here are five of the best to get you started.

Researcher Capital Preferences says super funds fail to appreciate the tension many retirees experience between their needs in their golden years and the size of their nest eggs.

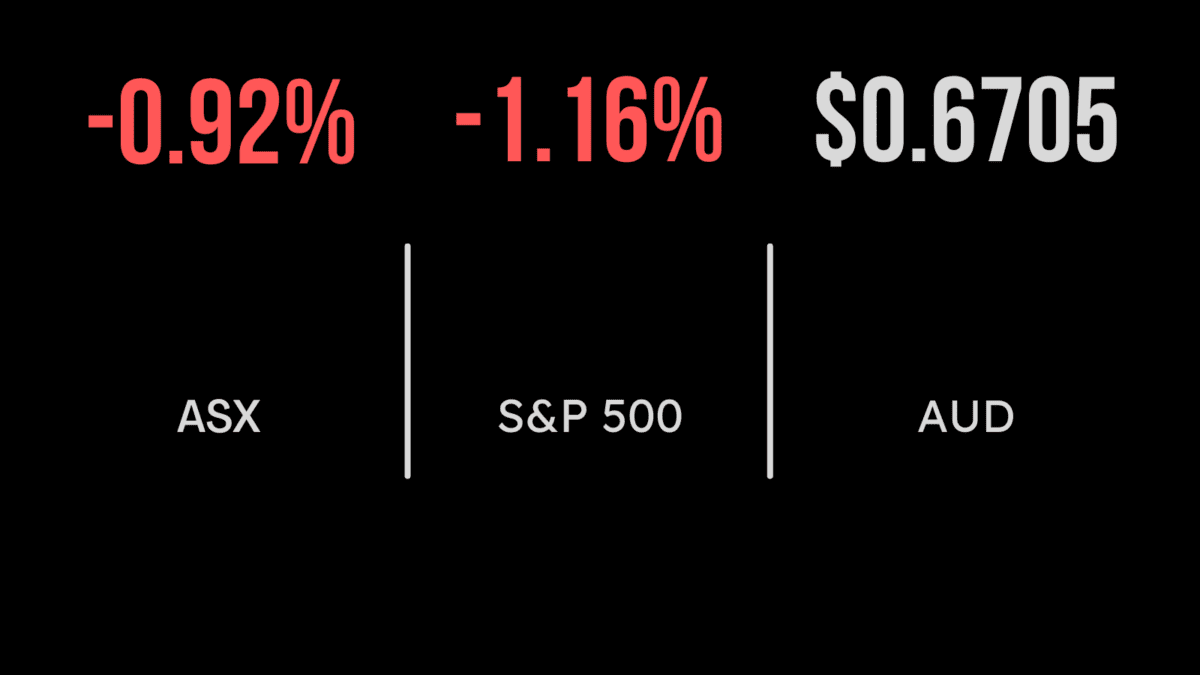

ASX snaps losing streak, Qantas cuts debt, Vulcan surges on big deal

The local market has reversed two straight weeks of losses, posting a 0.8 per cent gain on Friday which took the S&P/ASX200 to a weekly gain of 1.6 per cent.

The rally was powered by the unloved sectors in technology, property and retailers which were up 6, 2.5 and 2.2 per cent respectively as lower bond yields offered a reprieve to the market.

As has been the case all week, the only sectors that have not yet priced in the growing risk of an interest rate-led recession, being energy and materials, are now feeling the pain, with the sectors down 1.5 and 0.1 per cent on Friday.

Copper has hit a 16-month low, despite its important role in battery production while oil has officially entered a correction.

Qantas (ASX: QAN) fell 1.6 per cent after announcing they had managed to pay back $1.5 billion in debt while flagging an intention to cut capacity in 2023 in response to higher oil prices.

Vulcan Energy (ASX: VUL) was the standout, finishing 26.8 per cent higher after revealing massive vehicle manufacturer Stellantis had become the second-largest shareholder in the company.

Across the week the trend was the same with technology and property adding 8.1 and 7.1 per cent respectively, as Block (ASX: SQ1) gained 21.6 and REA Group (ASX: REA) 19.9 per cent.

The detractors were Lake Resources (ASX: LKR) and St Barbara (ASX: SBM) which fell 48 and 29 per cent each.

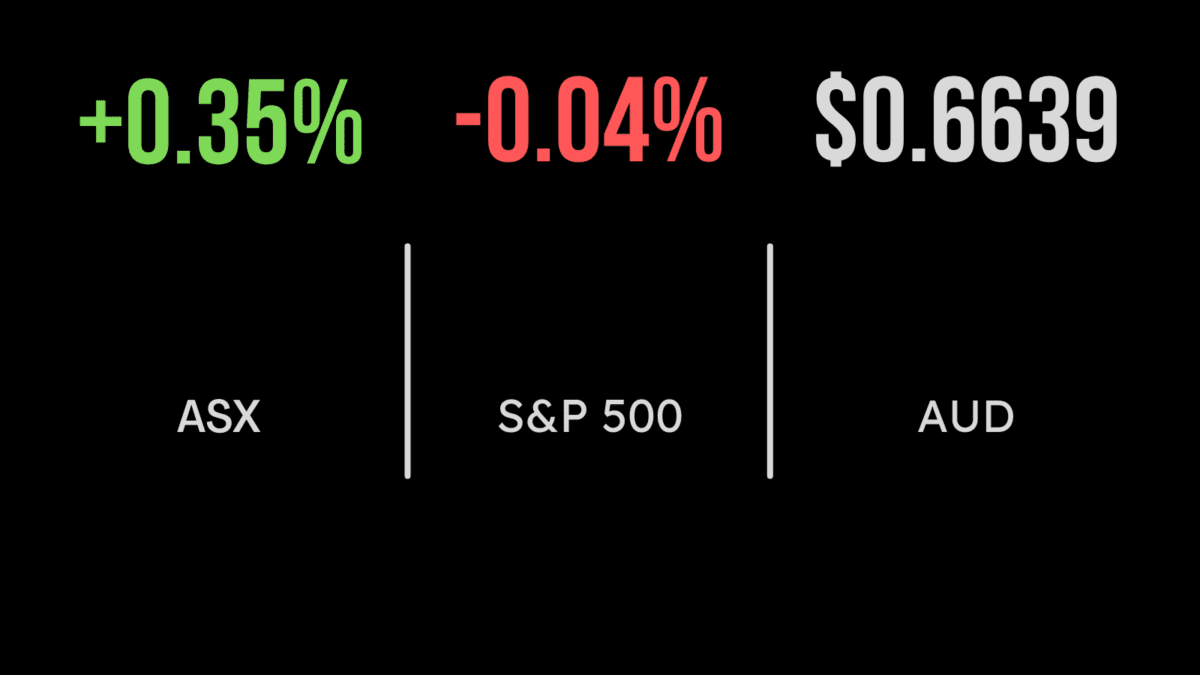

Global markets finish on strong note, FedEx upgrades, cruise lines gain

Global markets finished the week on an incredibly strong note, with the Dow Jones gaining more than 800 points to finish 2.7 per cent stronger on Friday.

The Nasdaq posted the strongest gain, up 3.3 per cent, with the S&P500 gaining 3.1 per cent as traders began considering the implications of recent rate hikes and pricing in multiple outcomes.

Among the most likely outcomes is a recession, triggered by demand destruction, which would likely benefit growth companies if it is accompanied by lower interest rates.

This realisation saw the bond yield fall during the week, benefiting tech and growth stocks but pushing the energy and materials sectors lower.

Inflation expectations have continued to fall and new home sales were unexpectedly strong.

In company-specific news FedEx (NYSE: FDX) gained more than 7 per cent after reporting an 8 per cent jump in revenue and profit ahead of expectations, suggesting the sale of goods could remain resilient.

Carnival Cruise Lines (NYSE: CCL) also brought the whole sector along with it, gaining 12 per cent after reporting second-quarter revenue that was 50 per cent ahead of the first on the back of a jump in occupancy from 54 to 69 per cent.

Markets gained the most since May 2020, with the Dow up 5.4 per cent over the 5 days, the S&P500 6.5 and the Nasdaq 7.5 per cent.

Top sectors hit by recession risk, bond yields fall, coal royalties

It is one of the most important facts to understand when investing in to share and bond markets but bears repeating; a market is a forward-looking machine.

That is, the daily activity and short-term trends in the market, are essentially explained as investors seeking to prepare for the future they expect.

This couldn’t have been more evident this week, as the recession talk reached a crescendo, but most global markets managed to deliver strong gains.

The selloff in most global markets has reached close to 20 per cent, or more than 50 per cent in high-growth stocks, with investors clearly positioning for high-interest rates and inflation for the foreseeable future.

However, the threat of recession this week saw sectors that you would expect to underperform, say retailers and property, deliver the strongest returns, primarily because the market had already priced in this risk.

The laggards in recent weeks have been the most popular sectors among professional investors for their ‘inflation hedge’ that being commodities and energy.

Having performed strongly when everything else fell, it was their turn to feel the heat. Talk of another commodity supercycle was brought back to reality with the copper price hitting a 16-month low and the oil price falling more than 10 per cent in a few short weeks.

The biggest surprise this week was likely news that the Queensland Government was adding an additional royalty payment for the extraction of coal where it is sold at today’s inflated prices.

This hit many businesses quite hard and likely reflects the short-termism that remains in government policy.