It can be hard to find good films starring older actors and about retirees. But it’s worth the reward when you find them. Here are five of the best to get you started.

Researcher Capital Preferences says super funds fail to appreciate the tension many retirees experience between their needs in their golden years and the size of their nest eggs.

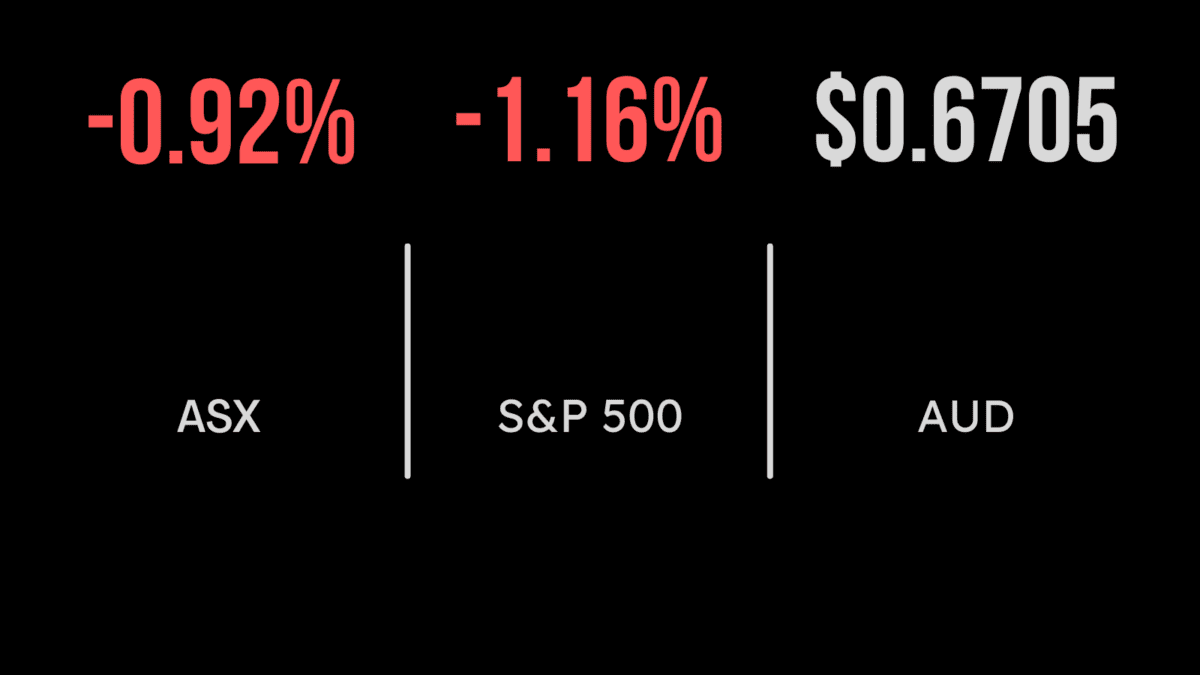

ASX finishes down 0.4 per cent as CSL drags

Market weaker despite positive lead, unemployment falls, CSL down on acquisition

The S&P/ASX200 (ASX: XJO) didn’t follow global markets higher, finishing down 0.4 per cent as CSL (ASX: CSL) dragged both the healthcare sector, down 5.1 per cent and the market lower.

The reason was the completion of their capital raising at an 8 per cent discount to the share price, which naturally sent shares down 8.2 per cent.

Management confirmed that institutions had delivered the $6.3 billion they were expecting for the Vifor purchase.

Most other sectors finished lower, but technology outperformed gaining 2.1 per cent behind the likes of Hub 24 (ASX: HUB) and Netwealth (ASX: NWL) which both moved 3 per cent higher.

This was despite a massive 366,000 in new jobs gained in the month of November sending unemployment down to 4.6 per cent and bond rates sharply higher.

ANZ Bank (ASX: ANZ) admitted to shareholders that they ‘got it wrong’ on their lending book, failing to capitalise on the booming loan market in 2020 and 2021 due to processing delays and technology.

Sticking with the banks, the Commonwealth Bank (ASX: CBA) finished 0.1 per cent lower and announced another 20-basis point increase to their five year fixed rate home loans.

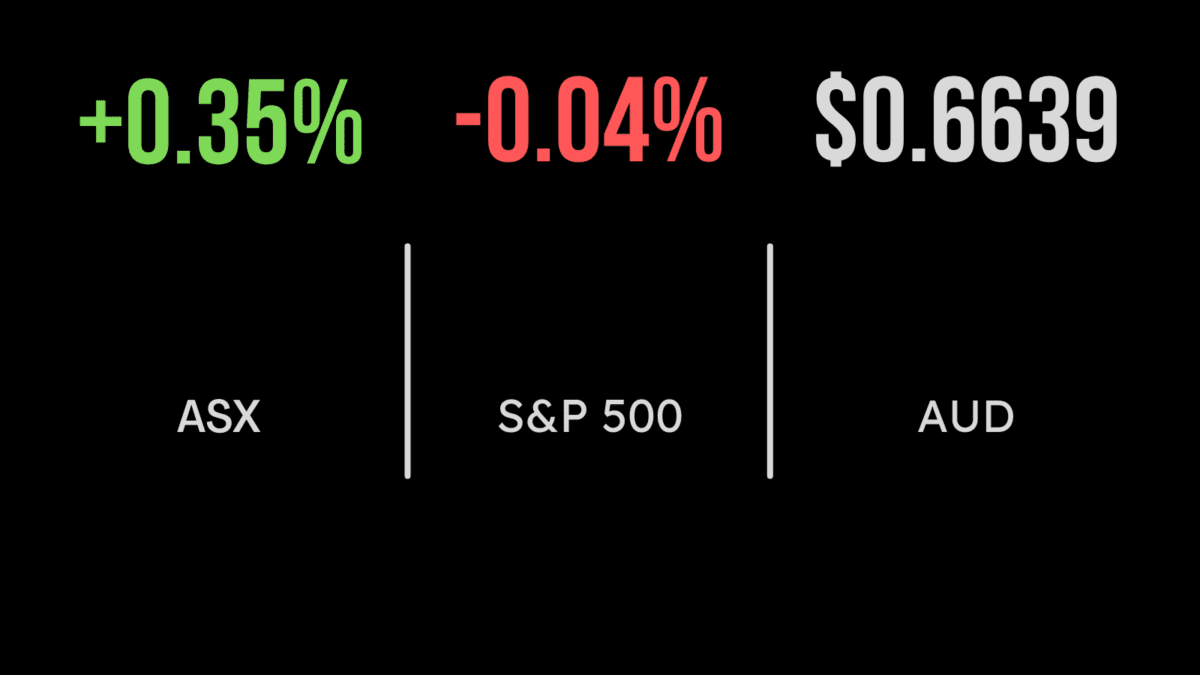

RBA speaks, Independence Group expands nickel assets, Qantas ready to pounce

The Reserve Bank Governor spoke for the last time for several weeks, once again reiterating that Australia was very different to the US.

He compared the 6.8 per cent US inflation rate to just 2.1 per cent in Australia, noting that this is the first time in six years it is even in the 2 to 3 per cent target band despite massive supply chain disruptions.

Bond buying is set to end in May 2022 should all go according to plan, but rate hikes are still at least back into 2023.

The ACCC formally approved the BHP (ASX: BHP) and Woodside (ASX: WPL) oil tie up, whilst IGO Limited (ASX: IGO) formerly Independence Group announced they had finalised a deal to buy nickel miner Western Areas (ASX: WSA) for an equivalent price of $3.36 per share.

This vastly expands their presence in the important sector for the decarbonisation trend.

Qantas (ASX: QAN) confirmed a slight improvement in their debt position, falling to $5.65 billion from a peak of $6.4 billion, with all 11,000 staff now back on deck.

They still expect a first half loss of up to $300 million but see domestic flights beyond COVID-19 levels before June.

Global travel is expected to recover more slowly, improving to 75 per cent in the second half.

First G7 rate hike, markets fall led by tech, Adobe tanks despite upgrade

Global markets reversed yesterday’s gains after the Bank of England somewhat unexpectedly became the first G7 nation to hike interest rates.

The Chancellor increased the cash rate from 0.1 to 0.25 per cent on concerns of sustained inflation which was sitting around 5.1 per cent.

This was bad news from global tech with many now expecting other major developed nations to hike rates sending the Nasdaq down 2.5 per cent.

The key detractors were Nvidia (NYSE: NVDA), down 6.8, Amazon (NYSE: AMZN) down 2.5, Netflix (NYSE: NFLX) down 2.3, and Tesla (NYSE: TSLA) down 5 per cent.

On the positive side the European Central Bank extended their bond buying program over the winter break, as they seek to support a slowing economy hit by the Omicron outbreak.

The Dow Jones finished flat and the S&P500 down 0.9 per cent as investors once again turn to more cyclical, short duration businesses.

Adobe (NYSE: ADBE) shares fell 10 per cent again despite reporting an increase in fourth quarter sales and over 20 per cent growth in both digital experience and digital media revenue.